NayaPay vs SadaPay: The last contrast for worldwide bills in Pakistan (2026)

Introduction: The rise of EMIs in Pakistan

For many years, Pakistanis struggled with international bills. NayaPay vs SadaPay Traditional banks frequently block transactions on websites like Netflix, Amazon, or OpenAI, citing “security issues” or complicated regulatory hurdles. iInputNayaPay and SadaPay. These EMIs acquired licenses from the country’s financial institution of Pakistan SBP, to simplify digital finance.

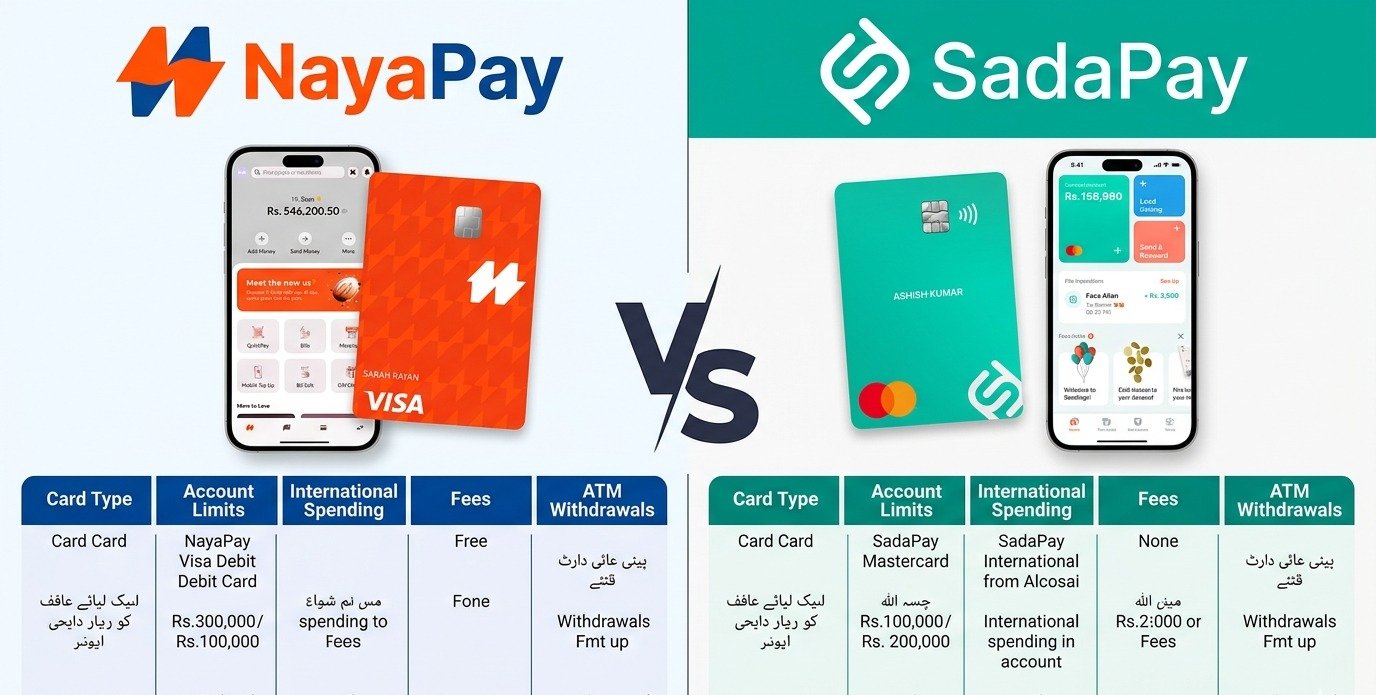

While each offers a virtual wallet and a debit card (Visa for NayaPay, credit card for SadaPay), they cater to barely distinct person reviews. In relation to global bills, the devil is within the information: trade rates, withholding taxes, and cross-border transaction expenses.

Part 1: NayaPay – The characteristic-rich Powerhouse

NayaPay, backed by the Lakson group, positioned itself as an “awesome App.” It isn’t only a card; it’s an ecosystem.

- The Visa gain

NayaPay offers a Visa virtual Card immediately upon registration and a physical Visa Debit card upon request. Visa is globally identified and regularly has a slightly broader acceptance rate in certain niche Asian and African markets as compared to credit cards.Worldwide transaction

- worldwide Transaction fees

NayaPay charges a fashionable percentage on worldwide transactions. In 2026, this generally levels among 3.five% to 5% (inclusive of the SBP-mandated withholding tax for filers and non-filers).

Filer: decrease withholding tax (WHT).

Non-Filer: huge tax hit on each worldwide dollar spent.

- POS and online international acceptance

NayaPay works seamlessly with:

marketing: fb ads, Google ads, LinkedIn ads.

Subscriptions: Netflix, Spotify, YouTube premium.

professional gear: Midjourney, ChatGPT Plus, Canva.

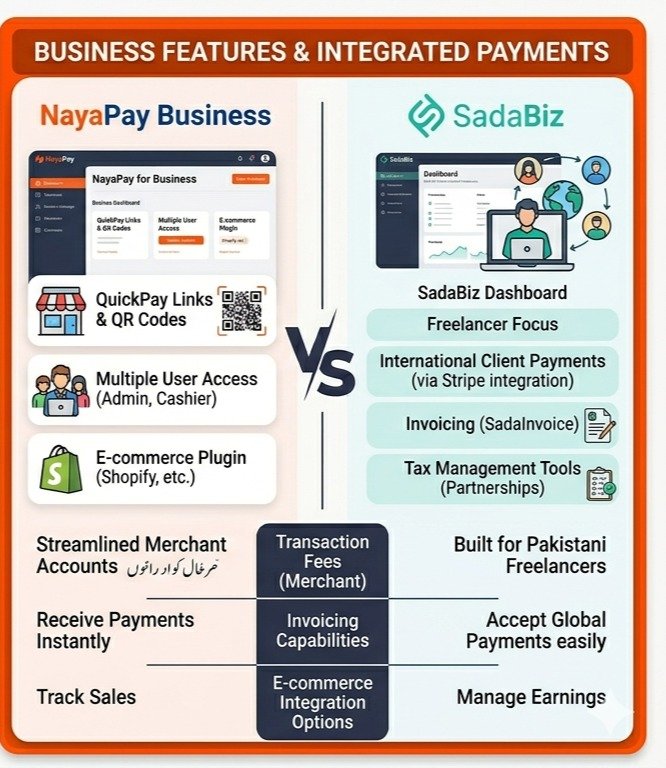

- The “Arc” enterprise Account

NayaPay introduced “Arc,” specifically designed for freelancers and small commercial enterprise owners. This permits better monthly limits (as much as 800,000 PKR or greater, depending on verification), which is imperative if you are purchasing high-priced international software programs or cloud hosting (AWS/Azure).

Part 2: SadaPay – The Minimalist’s Dream

SadaPay took the “less is more” technique. Their mission used to be to exclude the “hidden charges” associated with traditional Pakistani banking.

- The credit card factor

SadaPay makes use of the Mastercard network. For worldwide vacationers and online customers, credit card exchange rates are regularly noted as being marginally more favorable than Visa’s in the European and North American markets.

- The “No overseas Transaction charge” delusion vs. Truth

In its early days, SadaPay gained repute for having 0 forex markup. However, on account of SBP guidelines and foreign money volatility, they now fee a obvious rate. SadaPay’s aggressive side is its transparency—the app shows you exactly how a good deal was once charged as the base charge and what kind of tax it was once subject to.

- SadaBiz: The Freelancer’s Secret Weapon

SadaPay’s SadaBiz function is perhaps the satisfactory tool for worldwide bills in reverse—receiving cash. It lets freelancers generate invoices that customers will pay via deposit card or Apple Pay.

The benefit: The finances land in your SadaPay wallet at mid-market change rates, which you may then use to pay for your own global subscriptions.Part

part 3: Head-to-Head contrast for worldwide use

- trade quotes

trade quotes fluctuate every day. But, anecdotal evidence and consumer logs in 2026 advise:

SadaPay commonly remains toward the “interbank” charge plus a fixed percent.

NayaPay sometimes has a slightly better markup; it offers higher “instant refund” processing if a transaction fails.

- monthly Limits

NayaPay: primary money starts at two hund ed,000 PKR/month. Upgrading to an expert or commercial enterprise tier is easy if you provide source-of-income archives.

SadaPay: also begins at 2 hundred,000 PKR. Their SadaBiz tier is especially designed to handle large worldwide inflows and outflows.

- App stability and safety

while paying across the world, you do not need the app to crash during an OTP (One-Time Password) verification.

NayaPay: gives an especially impervious “Locked Card” function. You may keep your global payments toggled “OFF” and only turn them on the second you hit “Pay.”

SadaPay: regarded as the fastest UI. The “freeze card” feature is an unmarried faucet. Their 2FA (2-element Authentication) is especially reliable for 3-d invulnerable websites.

Part 4: Which one is better for unique Use instances?

1: The Freelancer (Winner: SadaPay)

If you are receiving payments from worldwide clients and the usage of that cash to pay for equipment like Adobe Creative Cloud or Upwork bid fast-monitoring, SadaPay (SadaBiz) is the winner. The ability to acquire cash via a simple link and the competitive trade price make it advanced for the “Earn-and-Spend” cycle.

2: the web shopper (Winner: NayaPay)

If you often shop on AliExpress, Amazon, or Shein, NayaPay often has higher promotional tie-ins. Their Visa card has a tendency to have fewer “declined transaction” issues on Chinese-language e-commerce platforms compared to Mastercard in certain regions.

3: The virtual Marketer (Winner: NayaPay)

Running Facebook or Google ads requires high limits and consistent “pings” from the merchant. NayaPay’s Arc business account provides the steadiness and documentation required to manipulate excessive-spend advert money owed without getting your card banned for “suspicious activity.”

Part 5: The “Hidden” expenses – Withholding Tax (WHT)

It is vital to remember that neither NayaPay nor SadaPay can waive the government of Pakistan’s taxes.

modern-day regulation: Any worldwide transaction is subject to WHT.

For Filers: 1% to 5% (depending on the 12 months’ budget).

For Non-Filers: 10% to 15%.

earlier than blaming your EMI for “stealing money,” take a look at your Filer reputation. each apps provide a clear breakdown of this tax in the transaction records.

Part 6: Customer Support in 2026

Whilst an international fee fails, and your cash is “caught” in a pending nation, help topics.

SadaPay: ordinarily chat-based. They’re famous for their “human” contact and lack of “bot” responses.

NayaPay: offers each chat and sturdy cellphone aid. For enterprise users, NayaPay’s smartphone assist is frequently quicker for resolving high-priced transaction blocks.

Part 7: Final Verdict

Pick out NayaPay if:

You need a comprehensive “magnificent App” for bills, bills, and enterprise.

You need a Visa card for precise service provider compatibility.

You’re an enterprise proprietor wanting higher documented limits (Arc).

You select having the option of smartphone-based customer service.

Pick SadaPay if:

You are a freelancer receiving international payments (SadaBiz).

You cost an easy, minimalist, and rapid person interface.

You want the most obvious breakdown of prices and taxes.

You decide upon theMastercardd community.

End: Why not both?

In 2026, the smartest method for a Pakistani freelancer or virtual nomad is to use each.

Use SadaPay to obtain your international profits at the first-rate prices.

transfer your “spending cash” to NayaPay to take advantage of Visa-exclusive promos or to keep your business costs separate.

Both NayaPay and SadaPay have revolutionized the financial landscape of Pakistan. They’ve forced traditional banks to improve their apps and give teens in Pakistan the electricity to take part in the global financial system. Whichever you select, you’re transferring far away from the “department-banking” headache and into the future of seamless international trade.

Are you a registered filer with the FBR? Understanding this will assist you in keeping up to ten % on every worldwide transaction you make with those cards!